If you are thinking about buying a new home shortly, you may already be searching online to get a feel for the different types of homes available in the local area. You may have reviewed your budget, and you may have a fair idea about a sales price that is comfortable for you to afford.

If you are thinking about buying a new home shortly, you may already be searching online to get a feel for the different types of homes available in the local area. You may have reviewed your budget, and you may have a fair idea about a sales price that is comfortable for you to afford.

While you may feel as though you have taken the preliminary steps necessary to prepare yourself to buy a home, it is important that you also get a mortgage pre-approval letter for your financing before you start hunting for that perfect new house or condo.

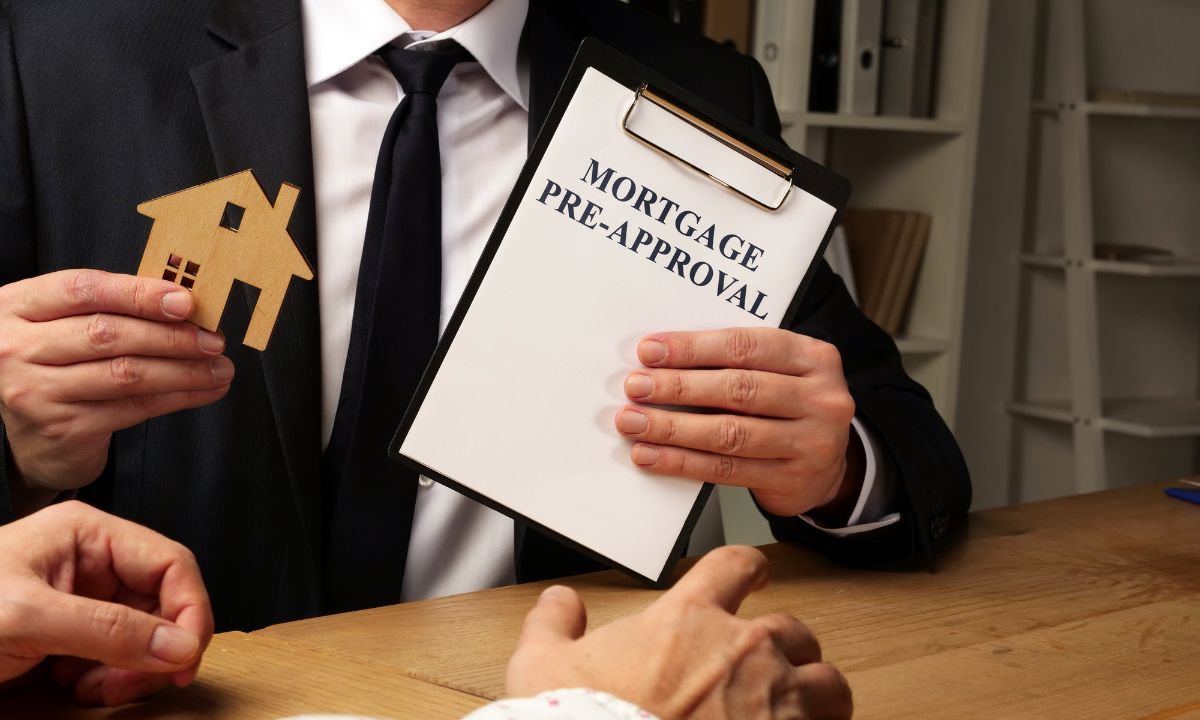

The Importance of a Pre-Approval Letter

A mortgage pre-approval letter is issued to a loan applicant after he or she has passed through a preliminary credit review process. Most of these letters state that the individual is pre-qualified for a property with a maximum sales price, and it is contingent on the loan applicant providing supporting documentation, such as tax returns and bank statements.

This letter gives you a better idea about what it will take for you to get final loan approval and what loan amount you may qualify for. The letter is also provided to a seller, and it gives the seller the confidence that comes with knowing that you are a qualified buyer. When a seller has an offer from a buyer with a letter and another offer from one without a letter, there is a good chance that the seller will opt for a buyer who is already pre-qualified for financing.

How to Get Your Pre-Approval Letter

As you can see, there are several reasons why it is important to get pre-qualified for your mortgage financing. Getting a pre-approval is generally a straightforward process, but it can seem intimidating. You will need to complete a loan application, and this may be done in person or online with a lender or mortgage company. You will also need to sign an authorization for the lender to pull your credit report. After taking these steps, you typically will be able to receive a pre-approval letter within a day or two.

When you have plans to purchase a new home, you likely will need to apply for financing to complete your plans. Getting a pre-approval letter up-front can help you in many ways, and you can easily take the steps necessary to get pre-approved for your mortgage. Simply contact a mortgage company or lender today to get started with the process.

Becoming a homeowner in a foreign land is an exciting yet intricate journey. For non-U.S. citizens, securing a mortgage in the United States involves understanding and meeting specific requirements. We will explore the essential prerequisites and considerations for non-U.S. citizens aspiring to own a piece of the American dream.

Becoming a homeowner in a foreign land is an exciting yet intricate journey. For non-U.S. citizens, securing a mortgage in the United States involves understanding and meeting specific requirements. We will explore the essential prerequisites and considerations for non-U.S. citizens aspiring to own a piece of the American dream. Have you finally found your dream home after months of searching, and then you are told that the seller has received other offers? No buyer wants to find themselves in a bidding war against another buyer as it is a stressful situation. Being unprepared and not having your finances in order will make it even more stressful. Here are a few quick ways if you’re looking to speed up your mortgage approval process, here’s a checklist to help you prepare:

Have you finally found your dream home after months of searching, and then you are told that the seller has received other offers? No buyer wants to find themselves in a bidding war against another buyer as it is a stressful situation. Being unprepared and not having your finances in order will make it even more stressful. Here are a few quick ways if you’re looking to speed up your mortgage approval process, here’s a checklist to help you prepare: There is a lot of jargon that comes with purchasing a home. Even though this could be confusing, purchasing a home is also a significant decision. Therefore, it is critical for everyone to understand exactly what they are signing before they scribbled their name on the dotted line. In some cases, a co-borrower or a co-signer (also called a non-occupying co-borrower) could be needed to strengthen the application. What is the difference between these two terms?

There is a lot of jargon that comes with purchasing a home. Even though this could be confusing, purchasing a home is also a significant decision. Therefore, it is critical for everyone to understand exactly what they are signing before they scribbled their name on the dotted line. In some cases, a co-borrower or a co-signer (also called a non-occupying co-borrower) could be needed to strengthen the application. What is the difference between these two terms?  Most people have heard the saying that it might be a good idea to refinance if mortgage rates drop. For those who might not know, refinancing is essentially taking out a new loan to replace the old one because the new loan has a lower interest rate.

Most people have heard the saying that it might be a good idea to refinance if mortgage rates drop. For those who might not know, refinancing is essentially taking out a new loan to replace the old one because the new loan has a lower interest rate.