It’s easy to get Private Mortgage Insurance (PMI) confused with homeowners’ insurance, but PMI is an entirely different thing that may or may not be necessary when it comes to your home purchase. If you’re going to be investing in a home in the near future and are wondering what PMI may mean for you, here are some things to consider regarding this type of insurance.

It’s easy to get Private Mortgage Insurance (PMI) confused with homeowners’ insurance, but PMI is an entirely different thing that may or may not be necessary when it comes to your home purchase. If you’re going to be investing in a home in the near future and are wondering what PMI may mean for you, here are some things to consider regarding this type of insurance.

Your Down Payment Amount

If you’ve been perusing the housing market for a while, you’ve probably heard that 20% is the ideal amount to put down when investing in a home; however, you might not realize why. The truth is that 20% down is the suggested amount because this will enable you to avoid having to pay PMI on the purchase of your home. In this regard, PMI is a protective measure for lenders since they may be taking on more financial risk with those who have less equity built up in their homes.

Getting Into The Market

For those who want to get into the real estate market right away and only have 10-15% to put down, PMI can be a means of being able to invest before mortgage rates increase. While buying a home when you want can certainly be a benefit, it’s also worth realizing that PMI is an additional fee and will impact the total cost of your home loan. It may be a risk worth taking if you want to buy now, but if it’s the total cost you’re considering, it may be better to save more before buying.

Getting Money Back

Whether you’re a homeowner or not, most people don’t look forward to tax time no matter how much money they get back. However, if you have PMI for your home, you’ll not only be able to get a variety of tax deductions, but you will also be able to get back some of the money that you invested into your private mortgage insurance. It may not be enough of a deduction to compete with saving up, but if you’ve found the perfect home the deductions can serve as an added incentive.

While you’ll only be required to pay PMI if you put down less than 20%, it can be a benefit if you’re looking to purchase a home right away. If you’re currently pursuing your options on the real estate market, reach out to one of our mortgage professionals for more information.

Today, we pause to honor the brave men and women who have served our country. Your courage, sacrifice, and dedication protect the freedoms that allow us all to call this nation home.

Today, we pause to honor the brave men and women who have served our country. Your courage, sacrifice, and dedication protect the freedoms that allow us all to call this nation home. When it comes to home financing, purchasing and refinancing a mortgage share similarities but serve distinct purposes. Understanding how each process works can help you make informed decisions about homeownership and financial planning.

When it comes to home financing, purchasing and refinancing a mortgage share similarities but serve distinct purposes. Understanding how each process works can help you make informed decisions about homeownership and financial planning. Planning to buy a home, finance a car, or cover unexpected expenses? Many loan options exist to help you achieve your financial goals, but choosing the right one can be challenging. Here’s a breakdown of the most popular types of loans, their unique characteristics, and what you need to know to make the best choice for your financial future.

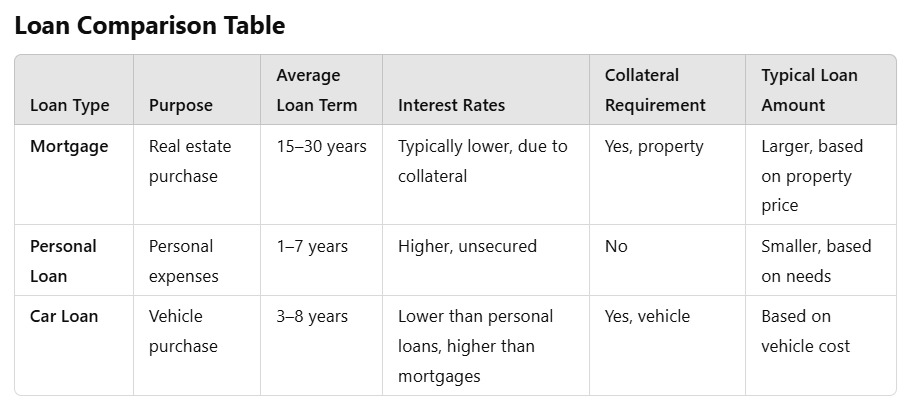

Planning to buy a home, finance a car, or cover unexpected expenses? Many loan options exist to help you achieve your financial goals, but choosing the right one can be challenging. Here’s a breakdown of the most popular types of loans, their unique characteristics, and what you need to know to make the best choice for your financial future.

If you’ve received your Closing Disclosure from your lender, congratulations! You’re almost at the finish line of your home buying journey, ready to celebrate with keys in hand. The Closing Disclosure, or CD, is provided at least three business days before your closing appointment and details your loan terms, projected monthly payments, and the much-discussed “cash to close.” But what exactly is “cash to close,” and how is it calculated?

If you’ve received your Closing Disclosure from your lender, congratulations! You’re almost at the finish line of your home buying journey, ready to celebrate with keys in hand. The Closing Disclosure, or CD, is provided at least three business days before your closing appointment and details your loan terms, projected monthly payments, and the much-discussed “cash to close.” But what exactly is “cash to close,” and how is it calculated?